Mandatory Convertible Bond Agreement: A Must-Know Instrument for Corporate Lawyers

BY : Anistya Pratista Rahma, SH

In assisting merger and acquisition transactions, corporate lawyers are often faced with various issues and concerns brought by the client. The need for capital, the concern over control and voting rights, and possible regulatory restrictions often emerge simultaneously in one transaction, encouraging corporate lawyers to think of creative and effective solutions to accommodate all these issues. In this article, we would like to bring up the Mandatory Convertible Bond (“MCB”) agreement, a hybrid debt security instrument as one of the solutions.

Why Use Mandatory Convertible Bond?

MCB is a type of bond that must be converted into a company’s common stock/shares on or before a specific future date. Unlike the traditional convertible bonds which give bondholders the option to convert, MCB requires the bondholder to convert the bond with equity upon specific time. MCB is a unique instrument, since it is started as debt, but ended as equity. The MCB holder will start off as a creditor, but upon conversion, they will become a shareholder.

A lot of multinational companies throughout times issued MCB, such as Bayer AG (German multinational pharmaceutical and biotechnology company), AT&T (world largest telecommunication company), Siemens Energy (German publicly traded energy corporation), and many more. In Indonesia, the issuance of MCB has also been done by a state-owned aviation company, Garuda Indonesia.

A discussion on the leverage of issuing MCB from the perspective of finance, investment, and corporate restructuring would be very lengthy, and various papers have discussed this thoroughly. The most common reason on why companies prefer to use MCB is that it offers them with immediate capital while delaying dilution of existing shares. Some also stated that MCB is used by companies, as it allows companies to raise funds without severely impacting their credit rating, since rating agencies usually treated MCB as equity rather than debt. MCB is also preferred compared to right issue, as issuing right issue may be perceived as indicative of a troubles or distressed situation. The reason would be endless, however, in this writing, the discussion would focus on why corporate lawyers should propose their client to use MCB Agreement, especially for transactions that involve foreign investors.

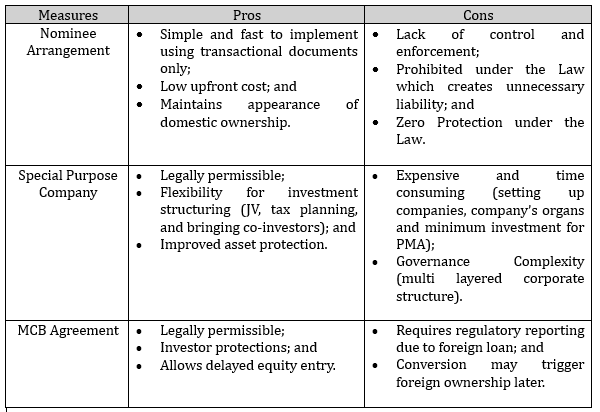

In Indonesia, foreign investments are usually imposed with higher standard requirements or even some restriction that limits corporate restructuring. For example, some sectors may limit foreign ownership up to certain percentage or even fully restrict foreign ownership. In other sector, foreign ownership would trigger higher standard, higher capital requirement, or any other specific requirements that are not required for domestic companies. To avoid foreign investor clients from being imposed with such restrictions, some of the most used measures are nominee arrangements and establishment of special purpose company.

However, both nominee arrangements and establishment of special purpose company have their own downsides. A nominee arrangement is an arrangement where a person (usually an Indonesian citizen) lends their name to be listed as the legal owner of an asset, including land or shares that is actually owned by someone else, i.e. the beneficial owner, often a foreign national, to circumvent legal restrictions on ownership. In Indonesia, nominee arrangement is essentially prohibited. Under Article 33 paragraph (1) of Law 25/2007, it is stipulated that:

“Domestic and foreign investors who invest in the form of a limited liability company are prohibited from entering into agreements and/or statements confirming that the ownership of shares in the limited liability company is for and on behalf of another person.”

Further, Article 33 paragraph (2) of Law 25/2007 stipulates that such arrangement will be deemed null and void. Further, the usage of nominee agreement also imposes a high risk to the investor, since the failure to appoint a trustworthy nominee would cause a wide range of problems in running the business.

On the other hand, the establishment of special purpose company, while being legally permitted, would require a lot of cost and time before the investor can run its business in Indonesia. The investor would be required to establish a limited liability company (perseroan terbatas), obtain necessary business licenses, maintain operational cost of the company, and comply with regulatory requirements in Indonesia. Given these shortcomings, an alternative solution for foreign investor is through MCB.

MCB enable foreign investors to inject its capital into a locally established company while maintaining certain degree of control over the local company’s business decisions. However, the rights and obligation of both foreign investor as MCB holder and the local company as MCB issuer shall be incorporated in a comprehensive MCB agreement. An MCB Agreement may stipulate wide range of rights and obligations of the foreign investors as the MCB holder of the local company. Unlike nominee arrangement, MCB agreement is not legally prohibited and will be recognized as ordinary agreement made based on the principles of freedom of contract, which is stipulated under Article 1338 KUH Perdata as follows:

“All agreements made in accordance with the law are binding on those who made them. Such agreements cannot be revoked except by mutual consent or for reasons specified by law. Agreements must be carried out in good faith.”

By entering the MCB agreement with foreign investor, a local company’s investment status would not immediately change to a foreign investment company. Thus, the issuer of MCB does not have to follow a foreign investment company requirement until the execution of the bond conversion, which may happen on a fixed date or the occurrence of certain event, as agreed between the parties.

Upon the subscription of MCB, foreign investors as the MCB holder may be entitled to certain rights as stipulated under the MCB agreement, which are the right to approve certain business decisions, receiving dividend in the form of coupon. Based on the above elaboration, the pros and cons of nominee arrangements, establishment of special purpose company, and the usage of MCB agreement may be summarized as follows:

While we are now able to identify the benefits of MCB as an alternative resort in facilitating foreign investments in Indonesia, we need a deeper knowledge on how MCB agreement must be made to facilitate the rights and obligation of the parties to ensure a smooth implementation of MCB. We will discuss the content of MCB agreement in a separate article.

Note: The content of this article does not constitute legal advice and should not be relied upon since there will be implemented regulations to be further issued. The judge's opinion may also be different, due to the facts relevant to the case. If you need specific advice related to this topic, please contact us by email at info@yangandco.com.